When managing business finances, understanding the documents that track your spending is essential. A cc statement, or credit card statement, serves as a comprehensive record of all transactions made using a credit card within a specific billing period. These monthly documents provide crucial insights into spending patterns, available credit, payment obligations, and account activity. For business owners, bookkeepers, and finance professionals, mastering the ability to read and analyze a cc statement represents a fundamental skill that ensures accurate financial tracking and informed decision-making.

What Is a CC Statement

A cc statement is a detailed monthly report issued by credit card companies that documents every transaction processed through your account. The term "cc" originates from "carbon copy" in traditional business correspondence, though in financial contexts, it commonly refers to credit card.

Key Components of Credit Card Statements

Every cc statement contains specific sections that provide essential information about your account activity and financial obligations.

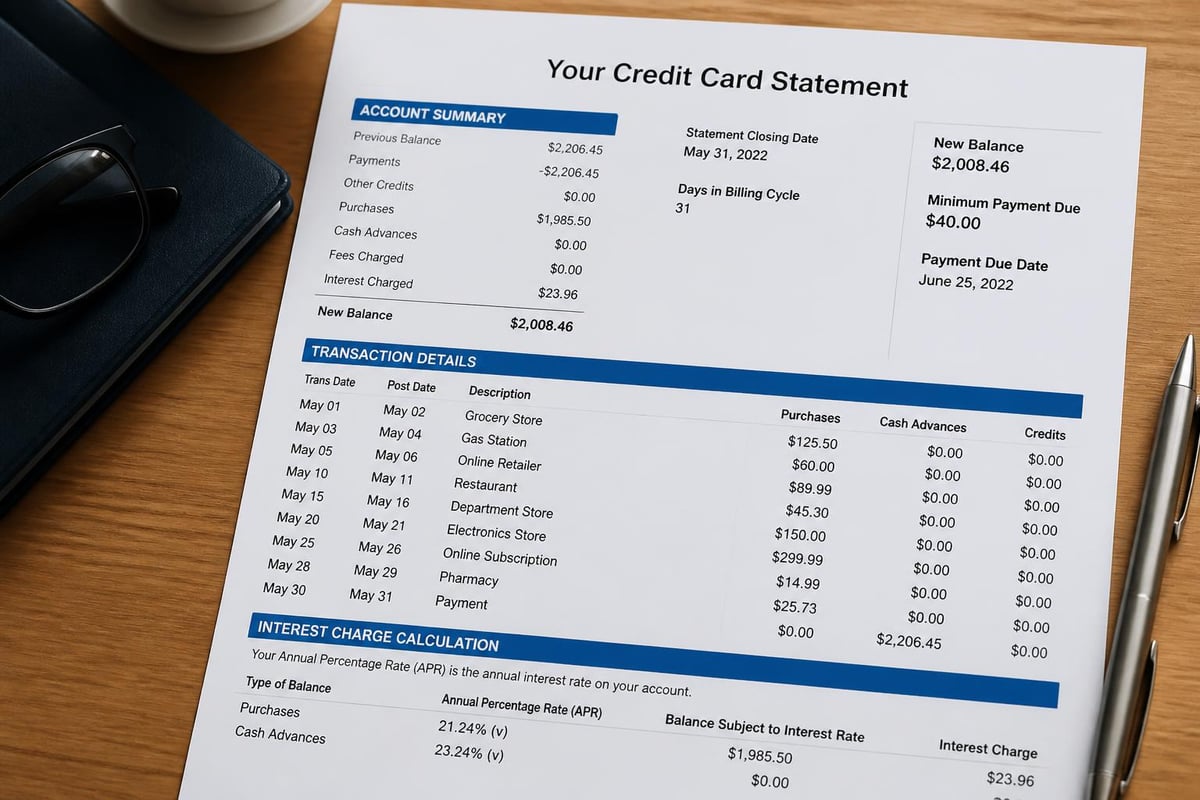

Account Summary Section displays your previous balance, new charges, payments received, credits applied, fees assessed, and current balance. This snapshot gives you an immediate understanding of your financial position.

Transaction Details list each purchase, payment, or fee chronologically or by category. These entries typically include:

- Transaction date

- Posting date

- Merchant name or description

- Transaction amount

- Category classification

Payment Information outlines your minimum payment due, payment due date, and total balance. Missing these deadlines can result in late fees and negative credit reporting.

Understanding Interest Calculations

The cc statement includes details about how interest charges are calculated on your outstanding balance. The Annual Percentage Rate (APR) determines the cost of carrying a balance from month to month.

Daily periodic rate is calculated by dividing your APR by 365 days. This rate applies to your average daily balance throughout the billing cycle. Understanding these calculations helps you make informed decisions about when to pay off balances versus when to carry them forward.

| Statement Element | Purpose | Business Impact |

|---|---|---|

| Previous Balance | Starting point for billing cycle | Tracks carry-over debt |

| New Purchases | Current period spending | Monitors expense patterns |

| Payments & Credits | Reductions to balance | Shows cash outflow |

| Fees & Interest | Additional charges | Impacts profitability |

| Minimum Payment | Required payment amount | Affects cash flow planning |

Why Accurate CC Statement Tracking Matters

Financial accuracy extends beyond simple record-keeping. A cc statement provides the documentation necessary for tax preparation, expense categorization, and budget compliance.

Tax Deduction Documentation

Business expenses charged to credit cards require proper documentation for tax purposes. Your cc statement serves as proof of purchase dates, amounts, and merchant information. Without accurate records, you risk missing legitimate deductions or facing challenges during audits.

Expense categorization becomes simpler when you regularly review your cc statement. Many business expenses qualify for different tax treatment, and proper classification ensures maximum tax benefits.

Fraud Detection and Dispute Resolution

Reviewing your cc statement monthly helps identify unauthorized transactions quickly. The faster you report fraudulent charges, the better protected you are under credit card regulations that limit liability.

Common red flags include:

- Unfamiliar merchant names

- Duplicate charges for single transactions

- Incorrect transaction amounts

- Charges from locations you haven't visited

- Subscriptions you don't recognize

Most credit card companies provide 60 days from the statement date to dispute charges. Regular statement review ensures you don't miss this window.

Reading Your CC Statement Effectively

Developing a systematic approach to reviewing your cc statement saves time and improves financial accuracy. Business owners should establish monthly routines that incorporate statement analysis.

Creating a Statement Review Checklist

Verification steps should include matching receipts to charges, confirming payment processing dates, checking for billing errors, and identifying unusual spending patterns.

Begin by comparing your cc statement against your own records. Many businesses maintain receipt files or digital expense tracking systems. Cross-referencing ensures every charge is legitimate and properly categorized.

Reconciliation Best Practices

Reconciliation involves matching your cc statement to your accounting records. This process identifies discrepancies before they compound into larger problems.

Monthly reconciliation should occur within days of receiving your cc statement. Prompt review allows time to dispute errors while details remain fresh. For businesses using accounting software, reconciliation features can automate much of this process.

When converting statements for accounting purposes, services that convert PDF bank statements to spreadsheets can streamline data entry and reduce manual errors, particularly when dealing with bank statement format PDF files from various institutions.

Digital CC Statements and Modern Banking

The shift toward paperless banking has transformed how businesses receive and manage their cc statement documentation. Digital statements offer several advantages over traditional paper versions.

Accessibility and Storage Benefits

Electronic cc statement delivery provides immediate access upon issue date. Rather than waiting for postal delivery, you can review charges within hours of the billing cycle closing.

Cloud storage integration allows businesses to maintain organized statement archives without physical filing systems. Digital statements are searchable, making it easier to locate specific transactions months or years later.

Security Considerations

While digital statements offer convenience, they require proper security measures. Protecting financial documents involves:

- Using strong, unique passwords for credit card account access

- Enabling two-factor authentication

- Storing downloaded statements in encrypted folders

- Regularly updating security software

- Avoiding public Wi-Fi when accessing financial accounts

Understanding email security terms like CC and BCC becomes particularly relevant when sharing financial information with team members or accountants.

Common CC Statement Errors and How to Address Them

Even with advanced processing systems, cc statement errors occur. Recognizing common mistakes helps you identify issues quickly.

Transaction Processing Errors

Duplicate charges happen when technical glitches cause a single purchase to post twice. Merchants may accidentally process transactions multiple times, or authorization holds may appear as actual charges.

Incorrect amounts can result from manual entry errors at point of sale. A decimal point in the wrong place can inflate charges significantly.

| Error Type | Typical Cause | Resolution Method | Timeframe |

|---|---|---|---|

| Duplicate Charge | System glitch | Contact merchant first | 1-3 days |

| Wrong Amount | Entry error | Dispute with issuer | 7-10 days |

| Unrecognized Merchant | DBA name difference | Verify receipt | Immediate |

| Missing Credit | Processing delay | Wait one billing cycle | 30 days |

Authorization Hold Confusion

Hotels, rental car companies, and gas stations often place authorization holds that may appear on your cc statement temporarily. These holds reserve funds but typically drop off within several days.

Understanding the difference between pending transactions and posted charges prevents unnecessary dispute claims. Posted transactions have completed processing, while pending items may still adjust.

Business Credit Card Statement Management

Business credit cards generate more complex cc statement documentation than personal cards. Multiple employees, varied expense categories, and higher transaction volumes require sophisticated management approaches.

Employee Card Programs

Businesses issuing cards to employees must track individual spending while maintaining overall account oversight. Your cc statement should provide transaction-level detail showing which cardholder made each purchase.

Spending limits and category restrictions help control expenses. Many business credit cards allow administrators to set individual limits for employee cards, preventing unauthorized spending.

Expense Report Integration

Modern businesses integrate cc statement data directly into expense reporting systems. This automation reduces manual data entry and improves accuracy.

Statement import features allow direct upload of transaction data into accounting platforms. Rather than manually typing each charge, finance teams can import entire billing cycles with a few clicks.

Converting CC Statements for Accounting Use

Financial professionals frequently need cc statement data in formats compatible with accounting software. Converting PDF statements to spreadsheets enables easier manipulation and analysis.

Data Format Challenges

Credit card companies issue statements in various formats, often as PDF files designed for reading rather than data processing. Extracting transaction details from these documents for accounting purposes traditionally required manual data entry.

Format inconsistencies across different credit card issuers complicate the conversion process. Each bank structures its cc statement differently, with varying column orders, date formats, and transaction descriptions.

Automated Conversion Benefits

Automated conversion tools extract transaction data from cc statement PDFs accurately and quickly. These solutions recognize common statement formats and structure data appropriately for accounting software import.

Benefits include:

- Reduced manual data entry time

- Minimized transcription errors

- Faster month-end closing processes

- Improved data consistency

- Better audit trail documentation

Understanding Statement Cycles and Due Dates

A cc statement covers transactions within a specific billing cycle, typically lasting approximately 30 days. Understanding these cycles helps you manage payment timing and avoid late fees.

Billing Cycle Mechanics

Your billing cycle start date determines when charges begin accumulating toward the next statement. The cycle close date marks when the issuer calculates your balance and generates the cc statement.

Statement closing occurs on a specific date each month, though the exact day may vary slightly. Transactions posted after the close date appear on the following month's statement.

Grace Period Optimization

Most credit cards offer grace periods during which you can pay your balance without incurring interest charges. Understanding your cc statement timing helps maximize these interest-free periods.

Strategic payment timing involves making purchases early in the billing cycle to extend the time before payment is due. A purchase made immediately after statement closing won't appear for nearly 30 days, then you have additional time until the payment due date.

Statement Analysis for Financial Planning

Beyond simple reconciliation, your cc statement provides valuable data for financial planning and business intelligence.

Spending Pattern Identification

Analyzing multiple months of cc statement data reveals trends in business spending. Seasonal variations, vendor concentration, and category shifts all become apparent through systematic review.

Month-over-month comparisons highlight unusual spending spikes or unexpected decreases. These patterns inform budget adjustments and identify potential cost savings opportunities.

Vendor Relationship Insights

Your cc statement shows how much you spend with individual vendors. This information supports vendor negotiation efforts and helps identify opportunities for volume discounts.

Payment method optimization involves determining whether certain vendors offer better terms for alternative payment methods. Some suppliers discount for ACH payments or checks versus credit card payments.

Regulatory Compliance and Record Retention

Businesses must retain cc statement documentation for specific periods to comply with tax regulations and industry requirements.

IRS Requirements

The Internal Revenue Service recommends keeping tax-related records, including credit card statements, for at least three years from the filing date. Some situations require longer retention periods.

Audit protection depends on maintaining comprehensive documentation. Your cc statement provides essential proof of business expense timing and amounts.

Industry-Specific Regulations

Certain industries face additional record-keeping requirements beyond general tax regulations. Healthcare, finance, and government contractors often must retain financial records for extended periods.

Compliance programs should include cc statement retention policies that meet or exceed regulatory requirements. Digital storage makes long-term retention practical and cost-effective.

Maximizing Credit Card Rewards Through Statement Review

Many business credit cards offer rewards programs tied to spending categories. Reviewing your cc statement helps ensure you're maximizing available rewards.

Category Bonus Tracking

Different spending categories often earn varying reward rates. Your cc statement categorizes transactions, allowing you to verify that purchases earned the correct bonus rate.

Rewards optimization involves using specific cards for categories that earn maximum benefits. Businesses operating multiple credit cards need systematic approaches to ensure each purchase uses the optimal card.

Redemption Timing Strategies

Your cc statement shows accumulated rewards balances and available redemption options. Strategic redemption timing can maximize value, particularly for travel rewards that vary in worth based on redemption method.

Understanding statement cycles helps time large purchases to meet minimum spending requirements for sign-up bonuses or promotional offers.

The Future of CC Statement Technology

Technological advances continue transforming how businesses receive, review, and utilize cc statement information. Artificial intelligence and machine learning now enable sophisticated analysis previously requiring manual effort.

Real-Time Transaction Alerts

Modern credit card programs offer real-time notifications for each transaction. While not replacing the comprehensive cc statement, these alerts provide immediate awareness of account activity.

Fraud prevention benefits significantly from instant alerts. Suspicious transactions can be blocked within minutes rather than being discovered during monthly statement review.

Predictive Analytics Integration

Advanced platforms analyze cc statement patterns to predict future spending, identify cost-saving opportunities, and flag anomalies automatically. Machine learning algorithms detect subtle patterns that human reviewers might miss.

Cash flow forecasting improves when historical cc statement data feeds into predictive models. Businesses can anticipate upcoming payment obligations more accurately and plan accordingly.

Managing your cc statement effectively requires consistent review, accurate record-keeping, and systematic reconciliation processes. Whether you're tracking personal business expenses or managing corporate credit programs, understanding statement components and developing solid review habits protects your financial interests and ensures compliance. When dealing with multiple financial institutions and varying statement formats, Bank Statement Boss simplifies the conversion process by transforming PDF credit card statements into organized spreadsheets compatible with your accounting platform, saving time while maintaining the accuracy your business demands.